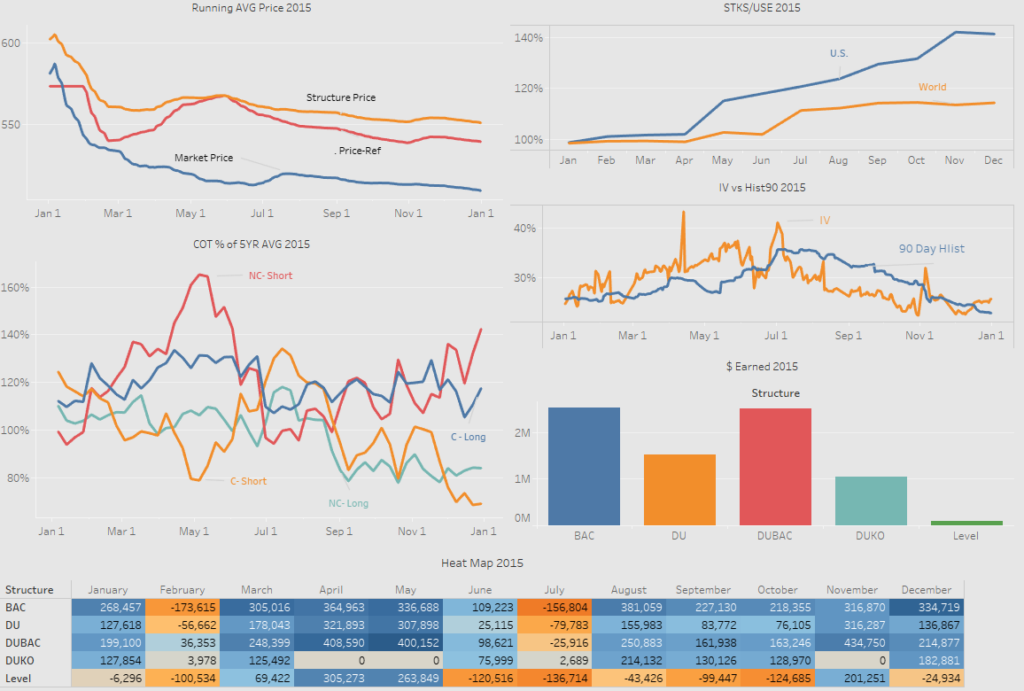

Wheat Market Snapshot

Large expected U.S. production numbers are putting pressure on prices as large yields are being seen as we get through harvest. However, forecasted tight stocks out of the rest of the world will keep a floor with potential to push prices up mid to long term if any export barriers are put up. The uncertainty looks to be widespread as the long & shorts are pretty eveningly distrubted between commercials and non commericals with the small increase of non commercial shorts likely due to price pressure due to U.S. harvest.

With implied volatlities off thier highs structured products are not going to be too sexy against the backdrop of a tight world supply against large U.S. production. None the less for producers looking to pick up 20 cents a bushel for a fixed volume while keeping some volumes open to pick the highs over the next 6 months a simple daily DU swap has the best value/risk proposition. Limiting the downside risk to the exisiting opportunity cost and having a cap that dissolves with time as the European wheat realities become more clear gives a good mix of downside protection, upside participation and sideways premium.

In 2015 there was a similar dynamic where U.S. production significantly outpaced world production causing a market dip as the U.S. harvest picked up. Then any pricing that protected against the down side would have been positative against the market and a few would have even consitantly bested thier reference prices. Still the main difference is the how much below the average world production is today with export bans as potential market events. Structures that have harsh limits on upside participation to cover a larger sideways premium could back fire.