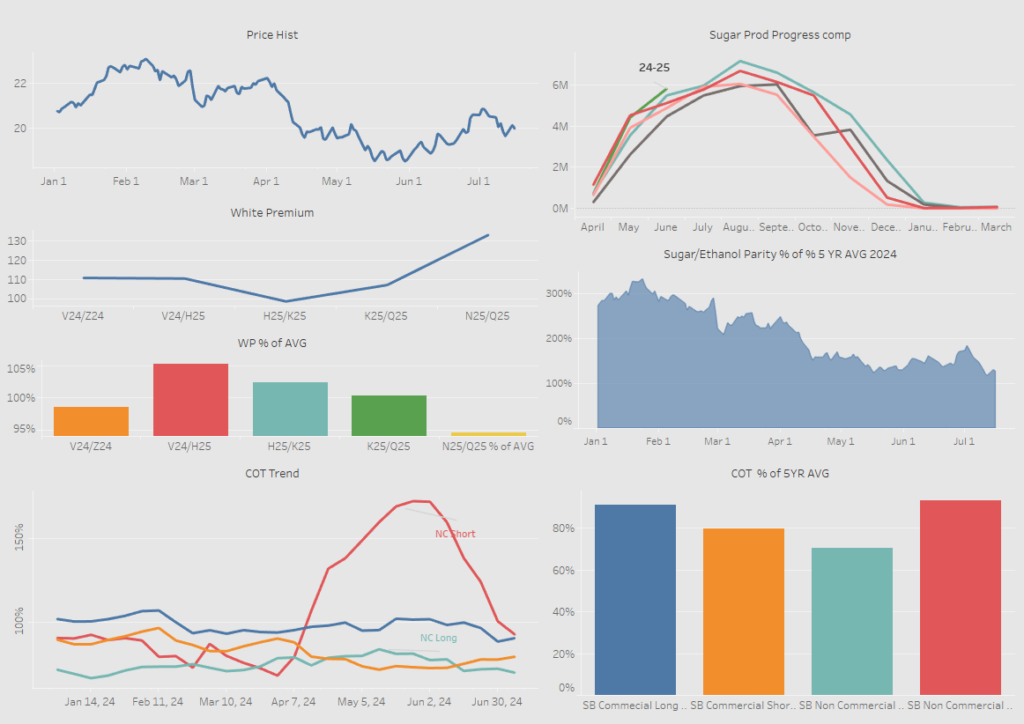

Sugar Market Snapshot

The Sugar market has a potential to be range bound as the Brazilian cane crushing season is ramping up. So far progress has even outpaced last years numbers with Sugar/Ethanol parity supporting raw sugar and hinting at large production numbers. However, with White Premium continuing to be good for Thai refiners and India putting a cap on exports there is little expectation of large raw sugar supplies outside of Brazil to hit the market putting a floor on prices going forward. This is echoed by the dramatic decrease in non-commercial shorts not wanting to take the chance on a production issue arising as Brazil’s milling season reaches its peak.

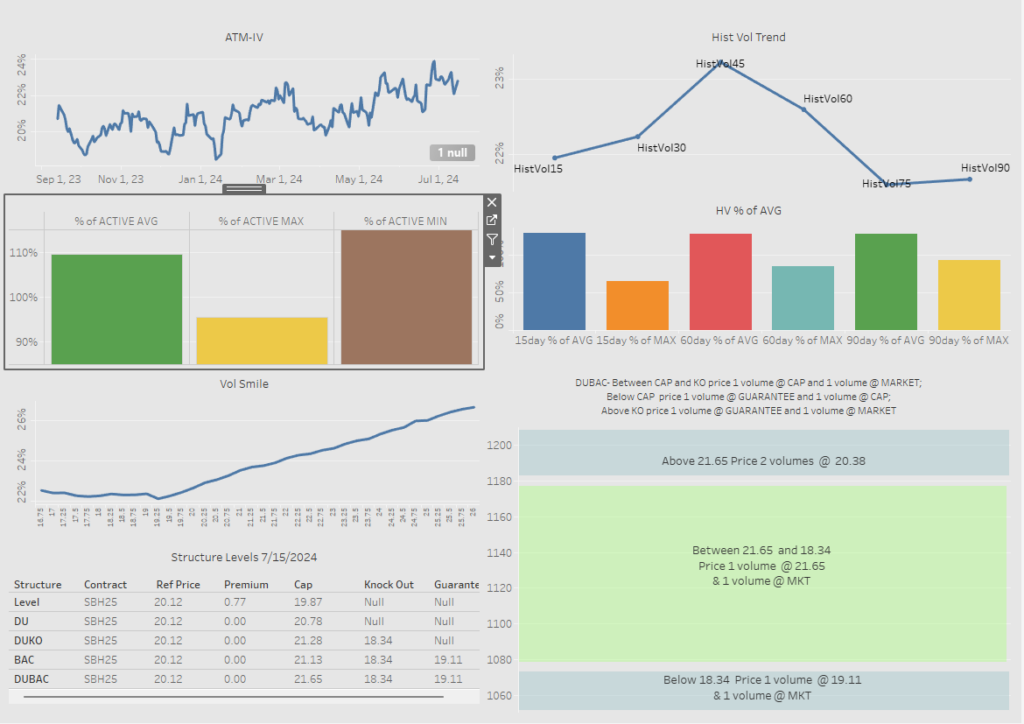

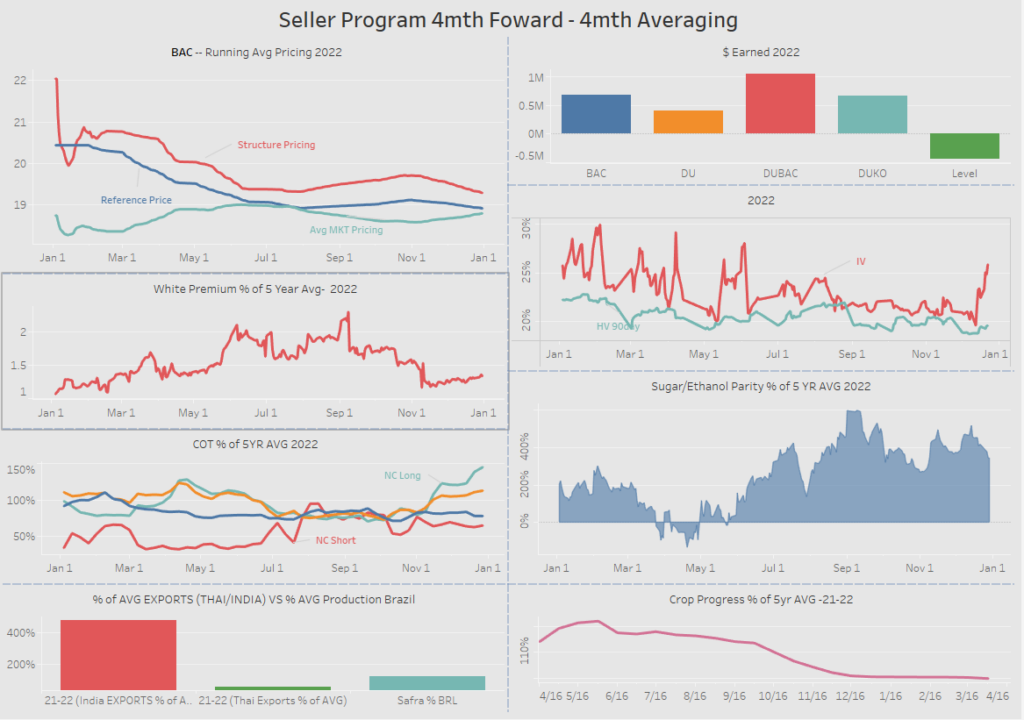

For producers looking to sell forward implied volatility is decent enough that you can collect daily over 1 cent if willing to accept some tail end risks that prices go down over the next 4 months. If there was a price over the next 2 weeks that one would pick, putting something around it with a Guarantee and some leverage, either daily or bullet, could be quite sexy.

In 2022 there was a similar market dynamic where Brazil was well above average in there prodcution period. However, without much Thai raw exports influenced by a robust white premium prices stayed ranged bound as Brazil’s milling season pushed along. A daily averaging leveraged product would have yielded between $500k – $1mm over selling the average price for a 5000 ton/month hedging program.

With no additional raw sugar suppplies expected out of Thailand or India the downside seems to be a tail end marco event with the upside leaning on the production pace of Central Brazil. Both of these provide a solid base for a steady range over the next 4-6 months that can be leveraged for some nice pricing options.